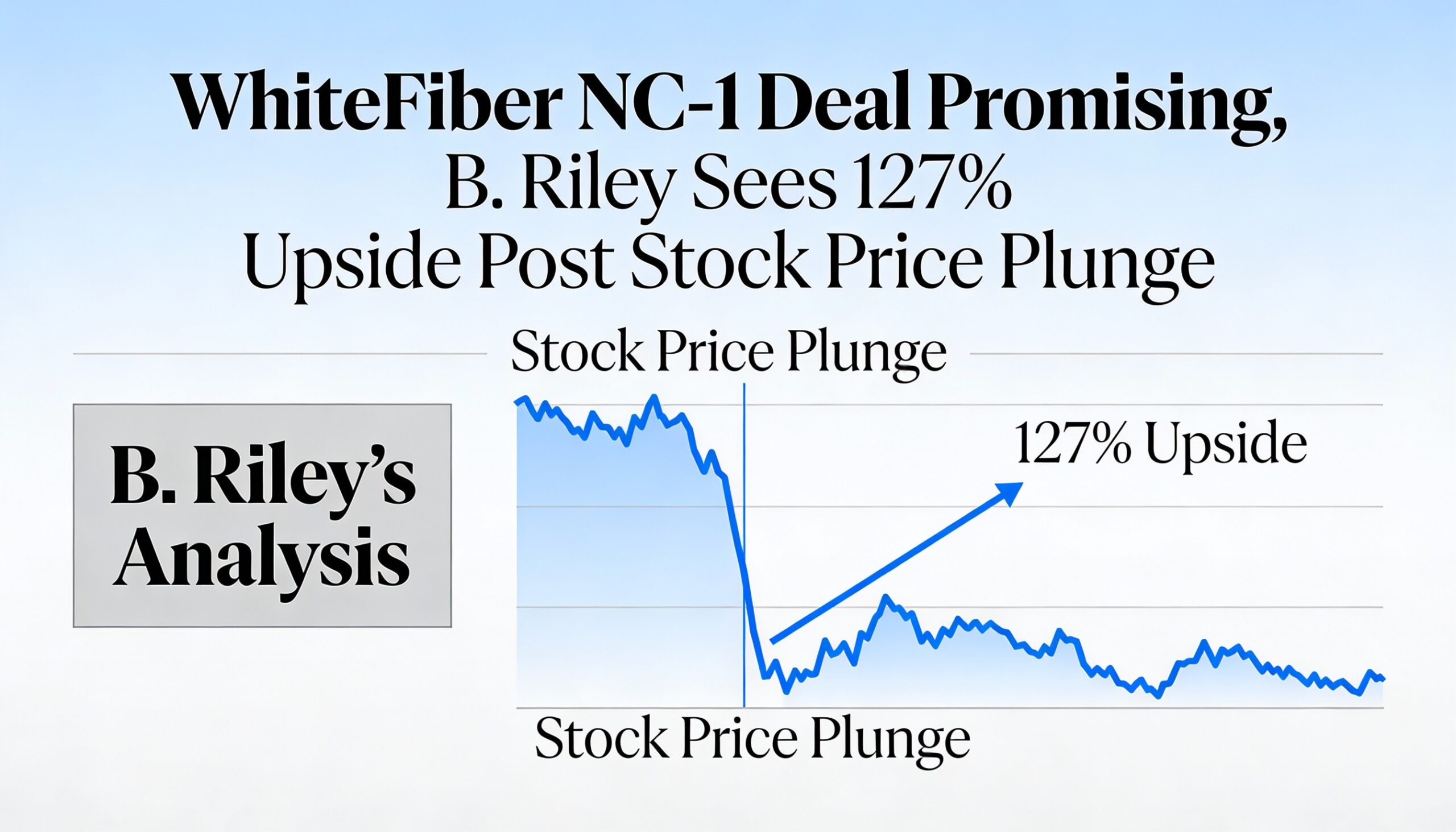

WhiteFiber’s inaugural long-term colocation agreement at its NC-1 campus marks an important validation of the company’s retrofit-led strategy, B. Riley said in a note on Tuesday.

The investment bank said the deal with Nscale Global demonstrates management’s ability to execute while staying on its original deployment schedule. Analysts Nick Giles and Fedor Shabalin wrote that reaffirming the timeline highlights both operational consistency and the advantages embedded in WhiteFiber’s retrofit model.

B. Riley maintained its buy rating on WhiteFiber (WYFI) but reduced its price target to $40 from $44, citing more conservative expectations for the Cloud Services segment. Even after the revision, the target suggests approximately 127% upside from the prior session’s close of $17.62. The stock is more than 50% below its record high reached about two months ago.

The analysts also noted that WhiteFiber is in advanced negotiations with lenders for a construction financing facility slated to close in early 2026. The facility may include an accordion option and credit enhancements, potentially lowering the company’s overall cost of capital.

From a valuation standpoint, B. Riley said WhiteFiber is trading at roughly 11 times its 2026 EV/EBITDA estimate and about 8 times EV/EBITDA based on its fourth-quarter 2026 adjusted EBITDA run rate, representing a sizable discount to peers that typically trade in the mid- to high-teens.