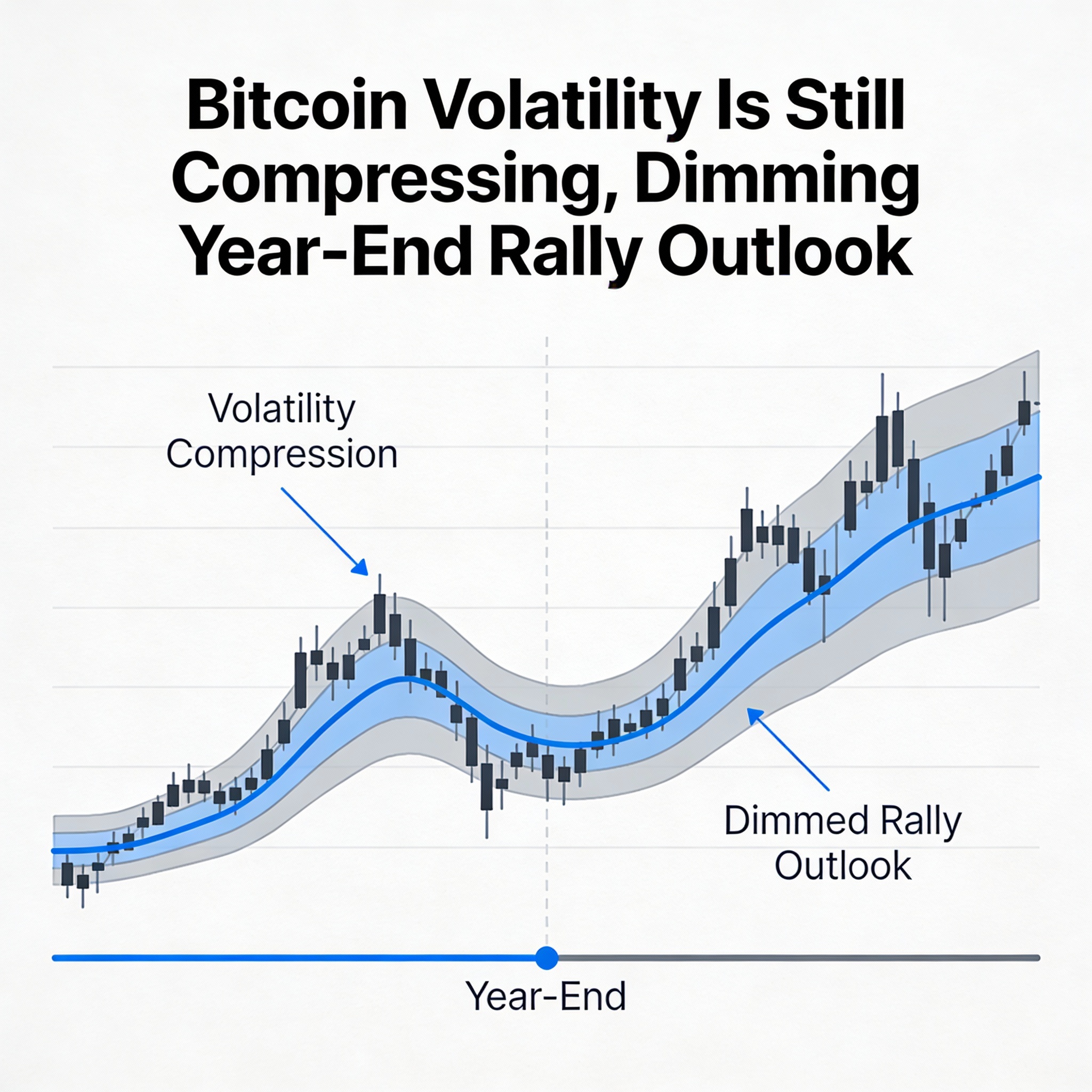

Bitcoin’s volatility is contracting, following a similar trend in the S&P 500, which is dampening expectations for a year-end rally.

BTC’s 30-day annualized implied volatility, measured by Volmex’s BVIV index, has dropped to 49%, reversing a surge from 46% to 65% over the 10 days through Nov. 21, according to TradingView. Lower implied volatility, derived from options pricing, signals reduced expected price swings over the near term.

The S&P 500’s VIX index has also eased, falling from 28% on Nov. 20 to 17%.

Matrixport said the ongoing volatility compression limits the probability of a significant year-end breakout. “With implied volatility continuing to compress, the likelihood of meaningful upside into year-end is reduced,” the firm noted. “The FOMC meeting is the last major catalyst, but volatility is expected to drift lower afterward.”

Historically, bitcoin’s price has tended to rise with volatility, though the correlation has shifted negative since November 2024. On Wall Street, periods of compressed implied volatility often precede bullish resets, highlighting mixed signals for bitcoin as the year closes.