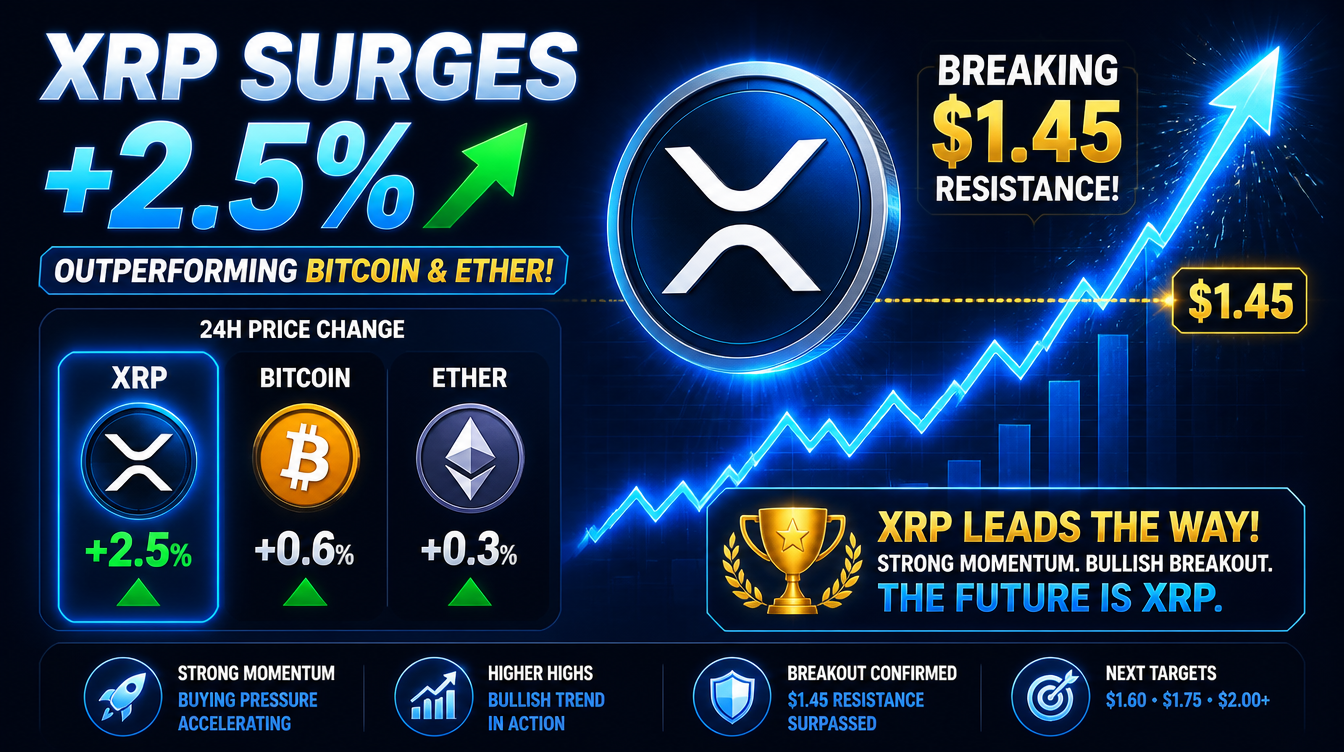

XRP delivered a decisive breakout above the $1.45 resistance level, supported by a sharp surge in trading volume that marked one of its strongest moves in recent weeks. The rally unfolded rapidly, indicating strong market participation, though momentum began to taper off as price approached the $1.50 psychological barrier.

Ahead of the move, XRP had been trading within a tightening range, with market participants anticipating a breakout as bullish patterns developed just below resistance. Low liquidity conditions across major exchanges increased the likelihood of a more pronounced price reaction once the level gave way.

Over the past 24 hours, XRP rose from $1.4176 to $1.4524, moving within a 6.5% range. The breakout intensified during the May 10 16:00–17:00 UTC window, when volume surged past 169 million and pushed the price above $1.4450.

The rally extended to a session high of $1.5073 before reversing back toward the $1.45 zone, as traders took profits near the peak. The rejection at $1.50 signaled the return of selling pressure, leading to a cooling of short-term momentum.

Despite the pullback, XRP continues to hold above its previous resistance area, suggesting the broader bullish structure remains intact. The $1.44–$1.45 range has now flipped into a key support zone, and maintaining this level will be critical for sustaining the breakout.

Looking ahead, $1.50 remains the immediate resistance after the failed attempt to hold higher levels. A sustained break above this threshold could reignite momentum, opening the path toward $1.56 and potentially the $1.80 level highlighted by analysts.

On the downside, a move back below $1.44 would weaken the current setup and increase the likelihood of a deeper retracement toward the $1.38–$1.40 range.