Tokenized silver futures briefly overtook bitcoin and ether as the largest source of liquidations across crypto markets this week, highlighting how macro-linked trades are increasingly driving volatility on digital-asset platforms.

The crypto-native silver contracts proved more volatile than bitcoin during the selloff, inflicting heavy losses on leveraged traders. Hedge fund manager Michael Burry, best known for “The Big Short,” described the episode as a self-reinforcing feedback loop in which falling prices triggered forced selling that pushed prices even lower.

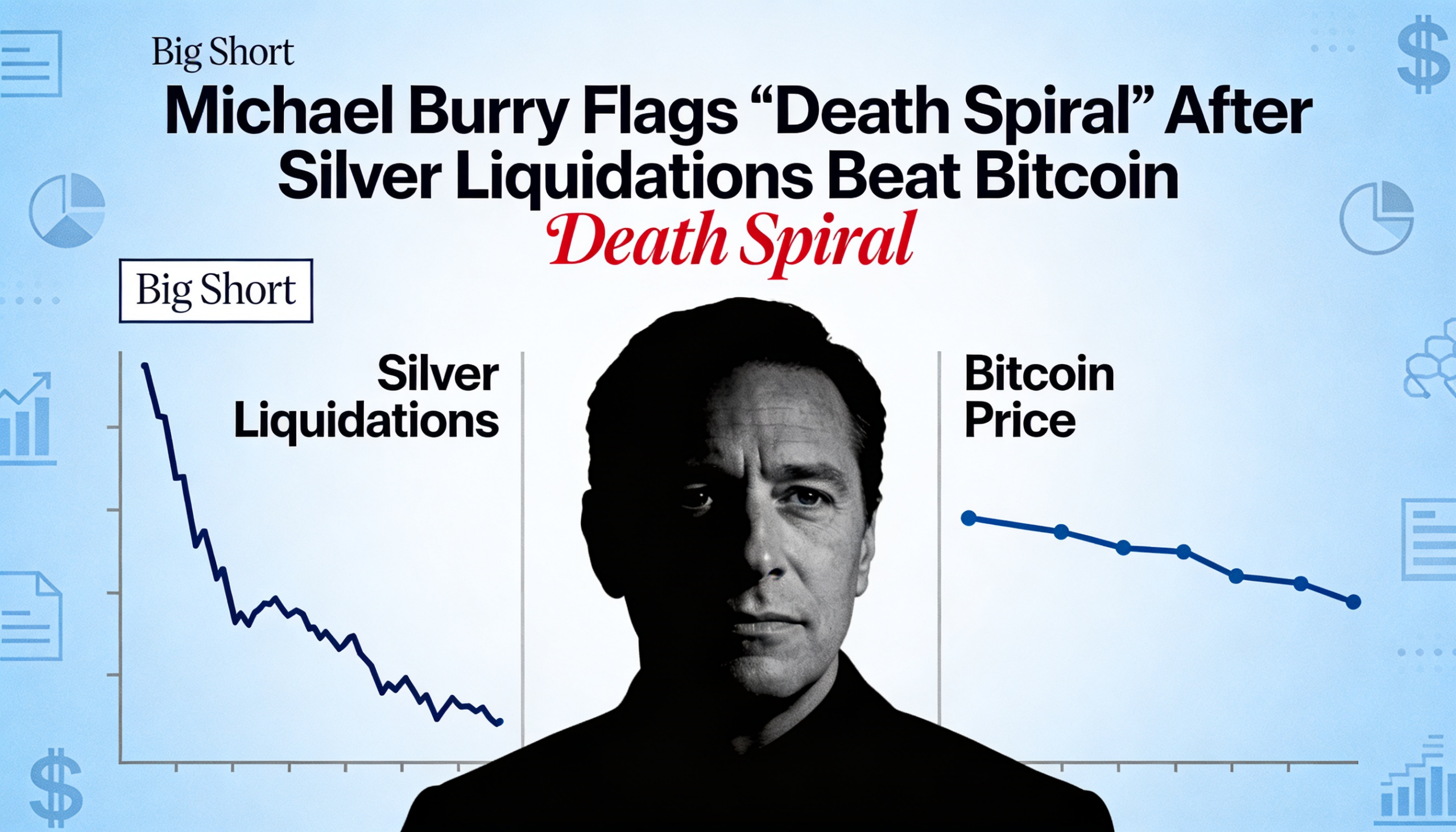

In a note this week, Burry characterized the move as a “collateral death spiral,” arguing that elevated leverage across crypto exchanges amplified the damage. As crypto collateral values declined, traders were forced to liquidate tokenized metals positions to meet margin requirements, accelerating the unwind.

“Sky-high leverage on these crypto exchanges tied to rising metals prices meant that as the crypto collateral fell, the tokenized metals had to be sold,” Burry said. “This is a collateral death spiral.”

Burry noted that silver-linked liquidations surpassed bitcoin liquidations on at least one venue during the episode. “It was reported that tokenized silver futures liquidations actually exceeded Bitcoin liquidations on one crypto market called, ironically, Hyperliquid,” he added.

The reversal was driven less by bitcoin-specific weakness and more by positioning in metals markets, where a sharp pullback collided with crowded leverage and thin liquidity. At the peak of the move, tokenized silver futures logged one of the largest wipeouts across crypto markets, eclipsing the usual liquidation leaders, bitcoin and ether.

Tokenized metals products allow traders to take directional exposure to gold, silver, and copper through crypto-native platforms rather than traditional futures exchanges. These contracts trade around the clock and typically require less upfront capital, making them attractive during volatile periods. That same structure, however, can accelerate forced selling when trades become crowded.

As metals prices rolled over, leveraged long positions were forced to unwind. Liquidations surged as traders failed to meet margin requirements or had positions automatically closed by platforms. On Hyperliquid, one of the most active venues for these instruments, silver-linked liquidations briefly exceeded those tied to bitcoin—an unusual moment in which a macro-linked contract became the primary driver of market stress.

The episode also coincided with tighter conditions in traditional markets. CME Group raised margin requirements for gold and silver futures, increasing collateral demands and pressuring leveraged traders to either post additional capital or cut exposure. While those changes apply directly to CME contracts, traders say shifts in positioning and risk appetite can quickly spill into tokenized markets that mirror the same underlying assets.

The broader takeaway is that crypto platforms are no longer used solely for crypto trading. They are increasingly functioning as alternative rails for macro exposure—and during periods of stress, that shift can upend liquidation dynamics in unexpected ways.